Trusts are versatile legal arrangements used for various purposes in Fiji, from managing assets for beneficiaries to carrying out long-term charitable missions. Whether you're looking to establish a foundation for community work, manage family wealth, or plan for succession, understanding how trusts are formed and recognised under Fijian law is crucial. While the most formal registration process applies specifically to Charitable Trusts seeking incorporation, other types of trusts also require careful setup and administration.

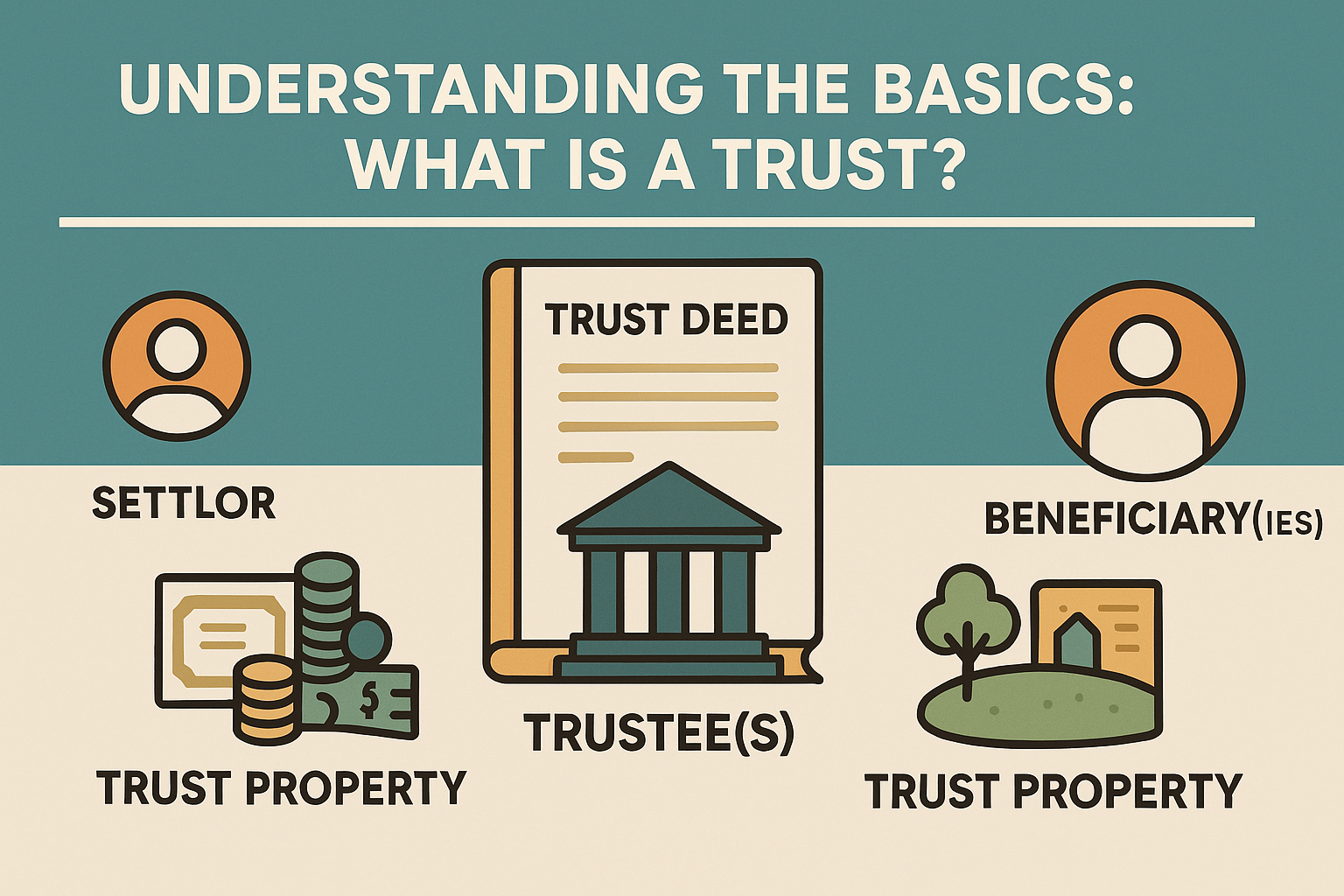

Understanding the Basics: What is a Trust?

At its core, a trust involves separating the legal ownership and control of assets from the beneficial ownership. Key elements include:

Settlor: The person or entity who creates the trust and transfers assets into it.

Trustee(s): The individual(s) or entity legally responsible for holding and managing the trust assets according to the trust's terms, for the benefit of the beneficiaries. They have fiduciary duties.

Beneficiary(ies): The person(s) or entity(ies) entitled to benefit from the trust assets or income.

Trust Property: The assets (e.g., money, shares, land) held within the trust.

Trust Deed: The critical legal document outlining the trust's purpose, powers and duties of trustees, identity of beneficiaries, how assets are managed, and the duration of the trust.

Types of Trusts and Registration in Fiji

The primary distinction in terms of formal registration relates to charitable versus private purposes:

Charitable Trusts: These are established for purposes deemed charitable under law (religion, education, poverty relief, community benefit etc.). To gain legal personality as a body corporate (allowing it to act like a company – own property, sue/be sued), a Charitable Trust must be formally registered under the Charitable Trusts Act (Cap 67) with the Registrar of Titles. This is the most common form of "Trust Registration" in Fiji.

Private Trusts (e.g., Family Trusts, Discretionary Trusts): These are typically created for private purposes like estate planning, asset protection for families, or managing assets for specific individuals (like minors). While they require a legally valid Trust Deed and adherence to general trust law principles and trustee duties, they are generally not registered as separate corporate entities under a specific Act like charitable trusts are. Their existence and operation rely primarily on the Trust Deed and compliance with common law and potentially other relevant statutes (like the Trustee Act).

This guide focuses primarily on the registration process for Charitable Trusts, as this is the pathway to formal incorporation.

Why Register a Charitable Trust?

Registering a Charitable Trust under the Act offers significant benefits:

Legal Personality: Becomes a body corporate, distinct from its trustees.

Credibility & Formality: Enhances public trust and simplifies dealings with banks, government, and donors.

Potential Tax Exemption: Registered Charitable Trusts meeting specific criteria can apply to FRCS for income tax exemption on funds used for their charitable purpose in Fiji.

Perpetual Succession: Can exist indefinitely, beyond the lifetimes of the original trustees.

For private trusts, the benefits lie more in achieving the specific goals set out in the Deed (asset protection, planned distribution) rather than public recognition or tax exemption.

Step-by-Step Registration (for Charitable Trusts)

The process involves applying to the Registrar of Titles under the Charitable Trusts Act:

Define Charitable Purpose: Ensure the Trust's objectives fall within legally recognised charitable categories.

Appoint Trustees: Select individuals (usually at least 3-5) to manage the trust.

Draft the Trust Deed: This foundational document must detail the Trust's name, objects, trustee powers/duties, governance, and provisions for winding up (distribution to other charities). Legal advice is strongly recommended.

Compile Application Documents: Gather the signed Trust Deed copies, application form, trustee details (IDs, police clearances often required), statement of assets, and pay the registration fee.

Lodge with Registrar of Titles: Submit the complete package.

Receive Certificate of Incorporation: Upon approval, the Registrar issues this certificate, confirming the Trust is a registered body corporate.

Setting Up and Operating a Registered (Charitable) Trust

After incorporation:

Obtain TIN: Register the incorporated Trust with FRCS for tax identification.

Apply for Tax Exemption: Make a separate application to FRCS demonstrating eligibility for income tax exemption based on charitable status and activities. This is not automatic.

Open Bank Account: Use the incorporation certificate and TIN.

Establish Governance: Implement procedures for meetings, record-keeping, and financial management as per the Trust Deed.

Compliance for Registered Charitable Trusts

Ongoing duties are vital:

Annual Returns: File returns with the Registrar of Titles, including updated trustee lists and audited annual financial statements.

Adherence to Purpose: Activities must remain strictly charitable.

Financial Accountability: Maintain proper accounts and manage funds prudently.

FRCS Compliance: Meet requirements to maintain tax-exempt status.

Considerations for Private (Non-Registered) Trusts

While not formally "registered" as bodies corporate, setting up and running a private trust still requires diligence:

Valid Trust Deed: Essential for establishing the trust's terms.

Trustee Duties: Trustees have strict fiduciary duties under law to act in the best interests of beneficiaries.

Taxation: Income generated by the trust and distributions to beneficiaries are subject to standard income tax rules. There is generally no tax exemption. Proper tax advice is crucial.

Record Keeping: Trustees must maintain clear records of assets, income, expenses, and distributions.

How Tax Pro Fiji Can Help Your Trust

Whether you are establishing a formally registered Charitable Trust or managing a private trust, sound financial management and tax compliance are essential. Tax Pro Fiji provides expert support:

For Charitable Trusts: We assist with obtaining the TIN, navigating the FRCS application process for tax exemption, setting up compliant accounting systems suitable for NPOs, and preparing financial reports for annual returns and audits.

For Private Trusts: We can advise on the tax implications for the trust itself, the settlor, and beneficiaries regarding trust income and distributions. We help ensure proper financial records are maintained for tax purposes.

General Trust Accounting: We offer tailored accounting and bookkeeping services suitable for various trust structures.

Ensure your trust operates on a firm financial footing and meets all its obligations.

Contact Tax Pro Fiji today for specialised financial and tax advice for your Fijian Trust.

Key Citations:

Registrar of Titles (Ministry of Justice): www.justice.gov.fj (Handles registration under Charitable Trusts Act)

Charitable Trusts Act (Cap 67): Via Fiji Laws website or Ministry of Justice.

Fiji Revenue and Customs Service (FRCS): frcs.org.fj (Handles TIN, Tax Exemption for charities, and general trust taxation)

Income Tax Act 2015: Sections on charitable exemptions and taxation of trust income/distributions.

Trustee Act (Cap 65): Outlines general duties and powers of trustees (relevant for all trusts).